June 2026

The rental markets in Australian capital cities are about to enter a period that housing policy makers need to carefully monitor.

The key insight from our analysis is that changes to rental growth or vacancy rates due to the delivery of additional supply is a positive policy outcome. These same changes to rental growth or vacancy rates due to a structural breakdown in demand, however, is a major red flag that will need immediate government attention.

Introduction

There has been a lot of recent discussion about auction clearance rates (and ultimately dwelling prices) given the announcement of the Federal Budget, rising interest rates and the war in the Middle East.

There has however been comparatively little commentary on the rental market. Recently, various data providers including SQM Research, Domain and Cotality released key rental data statistics – particularly around vacancy rates and rental growth.

This insight highlights that the rental markets are about to enter a critical period that housing policy makers need to carefully monitor. Changes to rental growth or vacancy rates due to the delivery of additional supply is a positive policy outcome. These same changes to rental growth or vacancy rates due to a structural breakdown in demand, however, is a major red flag that will need immediate government attention.

Understanding the rental market

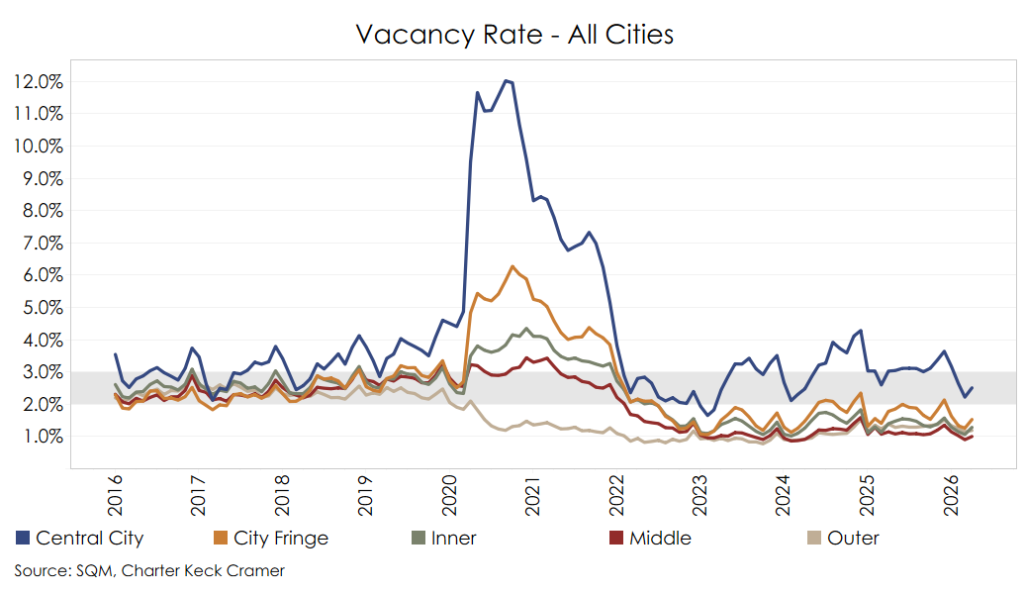

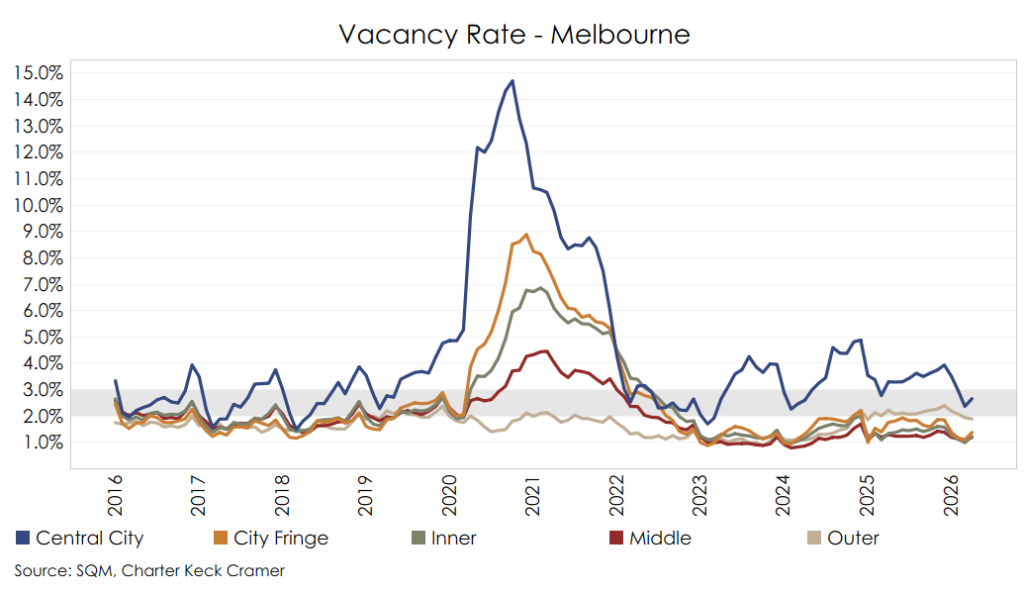

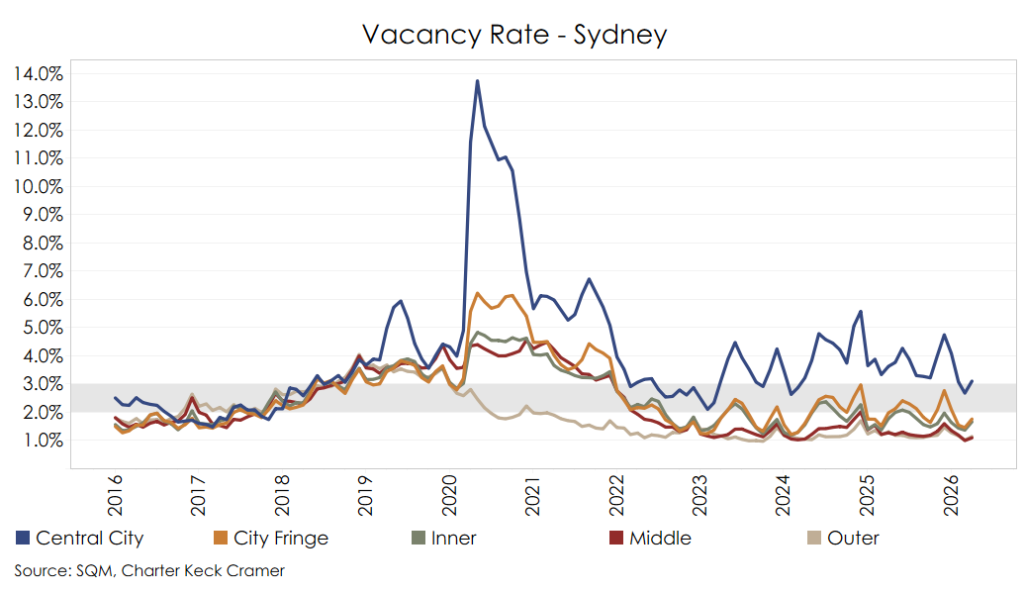

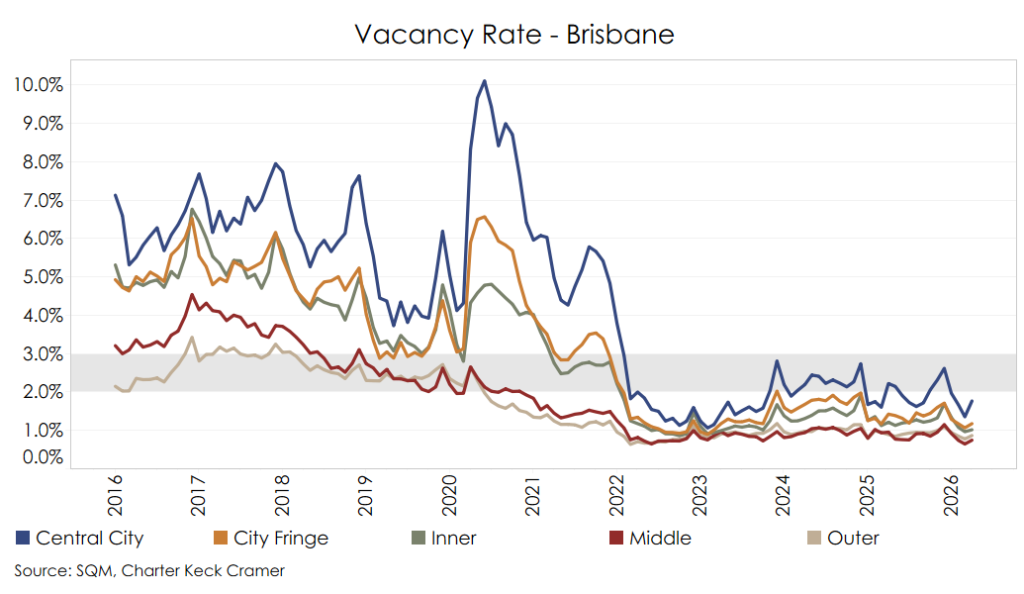

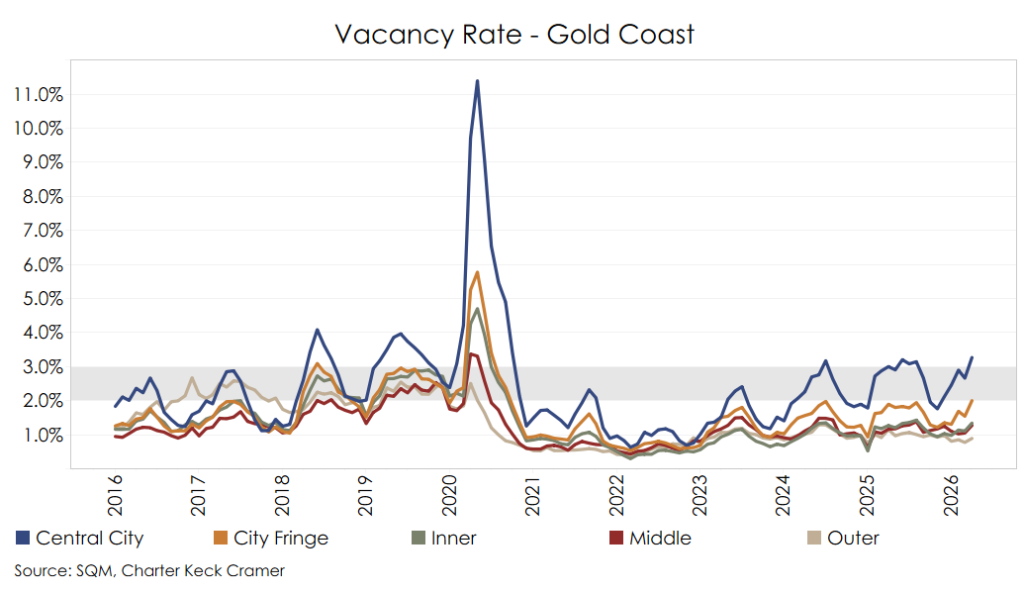

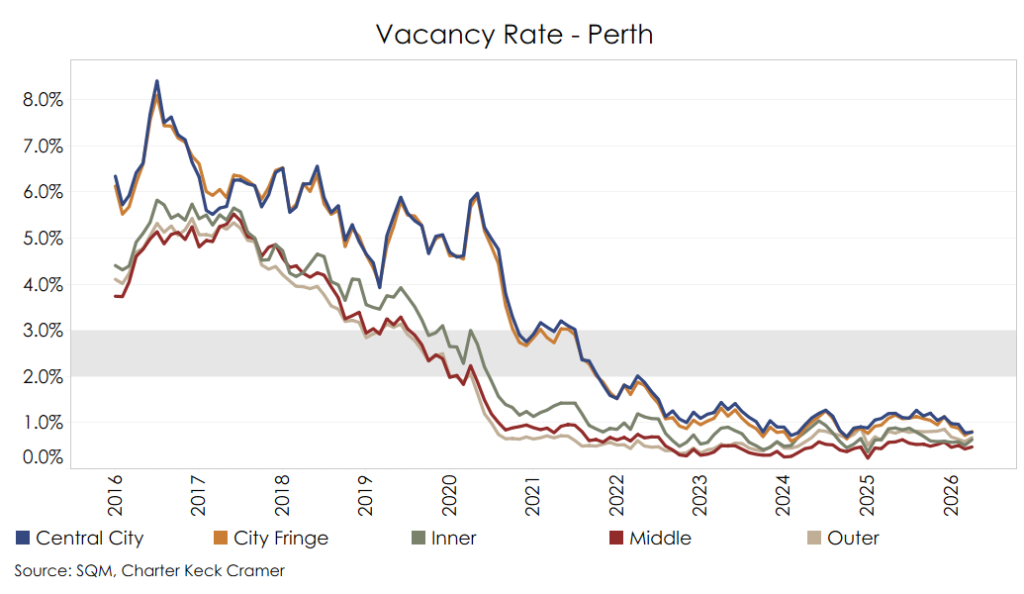

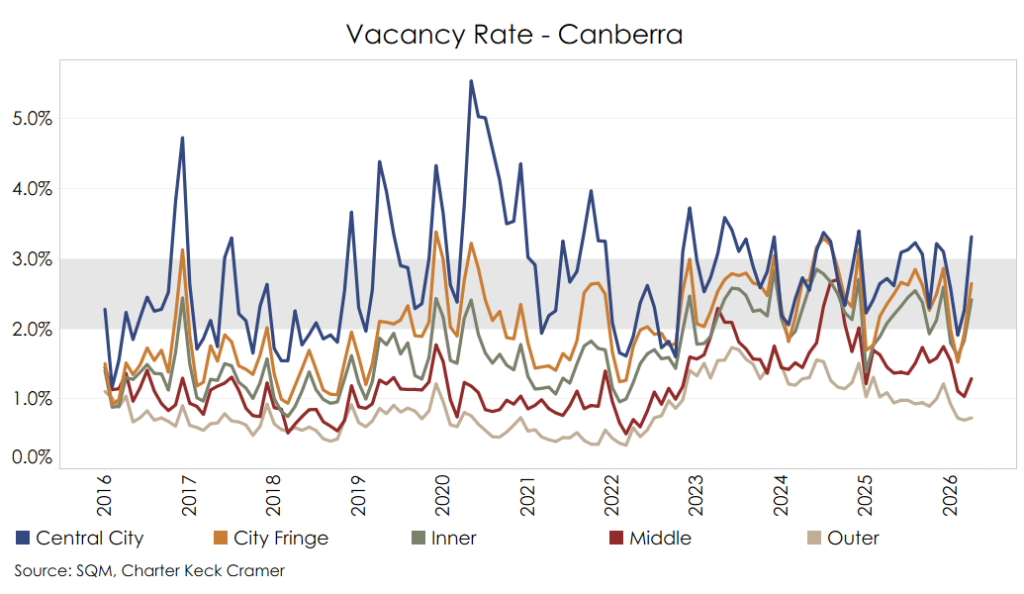

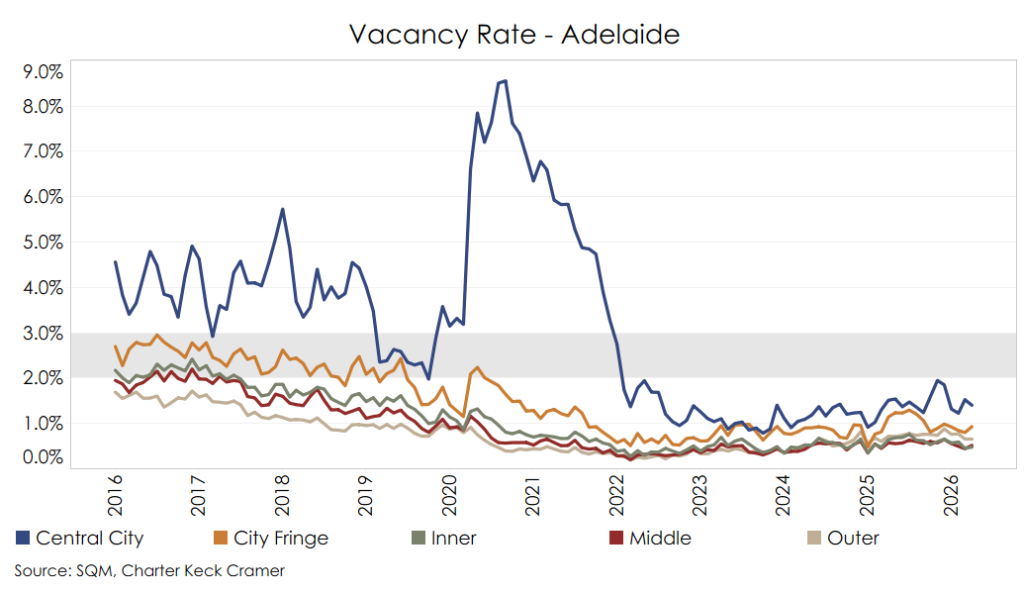

A simple, yet effective way to analyse the rental market is to consider the vacancy rate. A rental market is in equilibrium when the vacancy rate is broadly between 2% to 3%. At this point demand matches supply and rental growth is nominal or flat.

Additionally, in a balanced rental market, there is an inverse relationship between the vacancy rate and rental growth. A vacancy rate below 2% suggests a rental market is undersupplied and there will be outsized rental growth. The inverse is true when vacancy rates are above 3% with rental growth likely to underperform (or be negative).

Much like in the “For Sale” market, renters make trade-offs at different points in the market and economic cycles. These trade-offs include compromises between competing priorities such as rents vs location, size vs affordability, quality vs cost, or commuting time vs housing costs.

Dislocated rental markets

Prior to the release of the Federal Budget in May, every Australian capital city (other than Canberra) had chronically undersupplied rental markets. In fact, many of these rental markets were actually shrinking due to the increase or introduction of various taxes, charges and legislative requirements which was causing investors to divest their rental stock and exit the market.

The Federal Budget changes to negative gearing and Capital Gains Tax (CGT) are the biggest structural shift to Australia's residential investment landscape in more than a decade. The policy intent is clear: redirect investor capital from established stock into new construction.

Whilst this is well intentioned, our view is that these changes fail to fully consider the interrelationships and timing between the demand for dwellings and the supply of dwellings. Demand is very elastic and can change almost immediately, whilst new supply is inelastic and takes several months to several years to be delivered.

Furthermore, existing investors who sell established investment properties sell them to owner-occupiers who, by definition, will not rent them out. This reduces the rental pool.

With Australia's national rental vacancy rate at 1.2% in April, we cannot afford to lose rental supply at present.

So what does this all mean?

Our views are that the carve-out for new construction is the right instinct, however the timing simply doesn't work in the short term. The uncomfortable reality that few in government want to acknowledge is that it's going to make the rental crisis worse before it makes it better.

To be clear, this doesn’t mean that we feel that the reforms are wrong. After studying the markets, we note that structural reform always has transition costs and periods, and the long-term case for redirecting capital to new supply makes sense.

Policy makers do, however, need to be acutely aware of the short-term impacts of these changes to the rental markets and the fact that they may not behave as they would in a balanced environment.

Red flags to watch out for

Charter Keck Cramer have studied the rental markets through various market cycles and across all capital cities. We have observed with interest that the recent SQM Research statistics in fact show that there are certain sub-markets where vacancy rates are decreasing whilst rents are also decreasing. There are also other sub-markets where vacancy rates are increasing whilst rents are also increasing.

As set out above, this should not occur in a balanced housing market. The explanation is that the rental market is potentially breaking down on the demand side.

Most alarmingly, there are sub-markets such as Hendra (Brisbane), Summer Hill (Sydney), Hawthorn (Melbourne), Clayfield (Brisbane) and Lane Cove (Sydney) where vacancy rates are falling and rents are also falling. These sub-markets show signs of affordability ceilings being reached and are an example of demand destruction which is a very concerning structural pattern.

On the other hand, there are sub-markets such as Vaucluse (Sydney), Double Bay (Sydney), Balwyn (Melbourne) and Annerley (Brisbane) where vacancy rates have increased whilst rents have also increased. These are more luxury markets where wealthier tenants are vacating, and these properties are slowly being re-let at even higher rents.

Implications for policy makers

This is important behaviour for policy makers to closely monitor. Vacancy and rents changing through demand destruction is not the same as vacancy and rents changing through supply improvement.

One of these outcomes improves conditions for renters. The other just transfers the stress. Displaced tenants become crowded households, and crowded households become an affordability statistic that doesn't show up in vacancy rates.

To conclude, the rental markets are about to enter a critical period that housing policy makers need to carefully monitor. The data released over the next 6 to 12 months is critical to watch and will highlight if there are sub-markets with demand destruction which need to be addressed immediately.

As always, Charter Keck Cramer is here to assist with forward-looking and evidence-based research.

If you want more information, please don't hesitate to reach out to our Research team.